By the ISA

The global Islamic economy has burgeoned to an impressive $2.29 trillion in 2023. A significant part of this growth story is the transformative role of Islamic social finance. Rooted in principles of equity, charity, and social welfare, Islamic social finance is a beacon of hope and a practical solution in the fight against poverty. The Islamic economy isn’t just thriving in the newer modest fashion and digital entrepreneurship sectors, but it is also making substantial strides in ethical and socially responsible finance. Leveraging mechanisms such as Zakat (almsgiving), Sadaqah (voluntary charity), and Waqf (endowment), Islamic social finance has shown its potential to significantly impact poverty alleviation, especially in regions with substantial Muslim populations. In this article, we’ll explore how this ancient yet evolving financial system addresses one of humanity’s most persistent challenges: poverty.

Mechanisms of Islamic Social Finance

Islamic social finance, deeply rooted in Islamic principles, offers unique mechanisms for wealth distribution and social welfare. These instruments align with religious teachings and provide practical solutions for poverty alleviation and community development. Here, we explore the key instruments of Islamic social finance:

Zakat

The Pillar of Islamic Giving Zakat, one of the five pillars of Islam, is a mandatory charitable contribution calculated as a fixed proportion of a Muslim’s savings and wealth. As a compulsory act of worship, Zakat profoundly redistributes wealth and aids people in need.

It is estimated that if properly collected and distributed, Zakat has the potential to reduce poverty levels in Muslim-majority countries significantly. Today, Zakat is collected and distributed through various channels, including government bodies, NGOs, and digital platforms, ensuring a broader and more efficient reach.

Sadaqah: Voluntary Charitable Acts

Unlike Zakat, Sadaqah is a voluntary charity without any fixed amount or percentage, making it a flexible tool for social welfare. Sadaqah contributions often fund community projects, emergency relief, and other social welfare initiatives, directly impacting living conditions and providing support in times of crisis.

Waqf: The Endowment System

Waqf, an Islamic endowment of property or money for a specified philanthropic cause, has historically played a crucial role in developing Islamic societies. Modern Waqf systems are evolving, with initiatives like cash Waqf and corporate Waqf emerging, allowing for more diverse and sustainable social projects.

Qard Hasan: Interest-Free Loans

Qard Hasan refers to an interest-free loan provided for welfare purposes or to help someone in need, embodying the Islamic principle of helping others without seeking personal gain. These loans are particularly impactful in empowering low-income individuals or entrepreneurs who lack access to traditional banking services, thereby fostering economic growth and self-reliance.

Each instrument plays a vital role in the Islamic social finance ecosystem. They not only adhere to Islamic principles but also offer practical, ethical, and sustainable means of supporting social welfare and poverty alleviation. As the Islamic economy continues to grow, these mechanisms are increasingly being integrated with modern financial practices, expanding their reach and impact in addressing global socio-economic challenges.

Islamic Social Finance in the Modern World

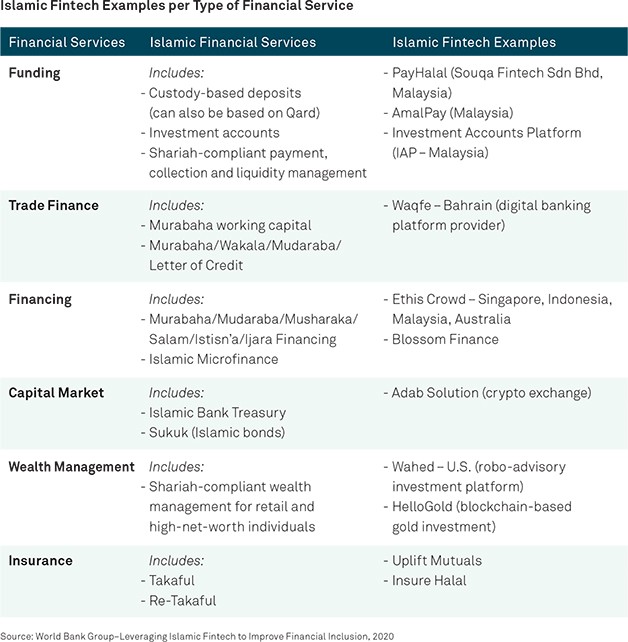

Adopting technology in Islamic social finance has streamlined processes, from the collection of Zakat to the distribution of funds. Digital platforms have enabled faster, more transparent, and more accountable transactions. Technology has also democratized participation in Islamic social finance, allowing individuals worldwide to contribute easily to Zakat, Sadaqah, and Waqf.

Fintech innovations in the Islamic finance sector have been pivotal in mobilizing resources. Digital platforms facilitate the efficient collection and allocation of funds, ensuring they reach the intended beneficiaries promptly and effectively.

Islamic fintech platforms play a vital role in financial inclusion, offering services tailored to the needs of the unbanked or underbanked populations, who often need financial support.

Case Studies: Islamic Social Finance in Action

As a crowdfunding platform focused on the global Muslim community, LaunchGood.com has been instrumental in supporting various causes, from disaster relief to community projects, showcasing the power of collective, community-based support. Platforms offering Islamic micro-financing and crowdfunding have opened new avenues for small-scale entrepreneurs and individuals in need. These platforms directly contribute to poverty alleviation and economic empowerment by providing interest-free loans and investment opportunities.

Platforms like Malaysia’s Ethis and Indonesia’s Evermos are prime examples of how Islamic social finance can be integrated into the business world. These platforms adhere to Islamic principles and support small and medium-sized enterprises (SMEs), fostering job creation and sustainable economic growth.

Impact on Poverty Alleviation

Islamic social finance has a tangible impact on poverty alleviation, addressing both immediate needs and long-term economic stability.

Direct Impact on Poverty Reduction

Zakat and Sadaqah provide immediate financial assistance to those in dire need, helping to alleviate poverty at the grassroots level. For example, in many Muslim-majority countries, Zakat collections amount to significant sums, directly supporting millions of impoverished individuals. Waqf endowments have historically funded educational institutions, healthcare facilities, and other community infrastructure, contributing to sustainable poverty reduction. Modern Waqf projects continue this legacy, often focusing on long-term community development. For example, the Waqfeyat Al Maadi Community Foundation (WMCF) in Egypt aims to create sustainable social impact through a longstanding but part-forgotten Islamic tradition.

Indirect Impact through Economic Empowerment

Islamic microfinancing and crowdfunding platforms have empowered countless entrepreneurs, particularly in underprivileged communities. These platforms enable individuals to start or grow businesses by providing interest-free loans and investment opportunities, creating jobs, and fostering economic independence. A study conducted in Indonesia showed that Islamic microfinance institutions helped increase the income levels of small business owners, demonstrating the indirect impact on poverty alleviation.

Challenges and Opportunities

While Islamic social finance has made significant strides, it faces several challenges that must be addressed to maximize its impact.

Challenges in Islamic Social Finance:

- Regulatory Hurdles: One of the primary challenges is the lack of a unified regulatory framework across different countries, which can hinder the efficiency and scalability of Islamic social finance initiatives.

- Limited Awareness and Understanding: There is still a significant gap in awareness and understanding of Islamic social finance mechanisms among both Muslims and non-Muslims, limiting participation and support.

Opportunities for Growth and Innovation:

- Technological Integration: The continued integration of technology offers immense growth opportunities. For instance, blockchain technology can enhance transparency and trust in the distribution of Zakat and Sadaqah.

- Global Partnerships: There is a growing opportunity for global partnerships between Islamic and conventional financial institutions to expand the reach and impact of Islamic social finance.

- Educational Initiatives: Increasing educational efforts to raise awareness about Islamic social finance can lead to greater participation and support, furthering its impact on poverty alleviation.

Conclusion

The unique combination of traditional Islamic principles and contemporary financial practices positions Islamic social finance as an effective tool for addressing poverty and promoting social development. Integrating Islamic social finance principles can create a more inclusive and equitable global economy. The path ahead for Islamic social finance is filled with potential and essential for fostering a balanced and just economic system worldwide.

Courtesy: The Islamic Services of America (ISA) is a leading authority in Halal certification within the United States and North America.